With Labor Day in the rearview and the NFL season underway, we mark the passing of Summer into Fall and, of course, overlooked news from the week for you, the community FI leader.

This week, we look at primary research on consumer banking from J.D. Power.

Banking consumer survey results

J.D. Power released their most recent survey of 4,000 U.S. retail banking consumers. While overall consumer financial health isn’t improved, concerns around inflation are high, but decreasing.

For a third consecutive month, the number of bank customers who say that the cost of goods is increasing faster than their income decreased. Nearly two-thirds (66%) of customers say they are struggling to keep up with the cost of goods, which is the lowest level this calendar year by far.

Tools are failing those who need them most

The tepid opinion of tools provided by banking providers may be more direct and actionable. Most consumers found their primary institution’s tools confusing and lacking insights.

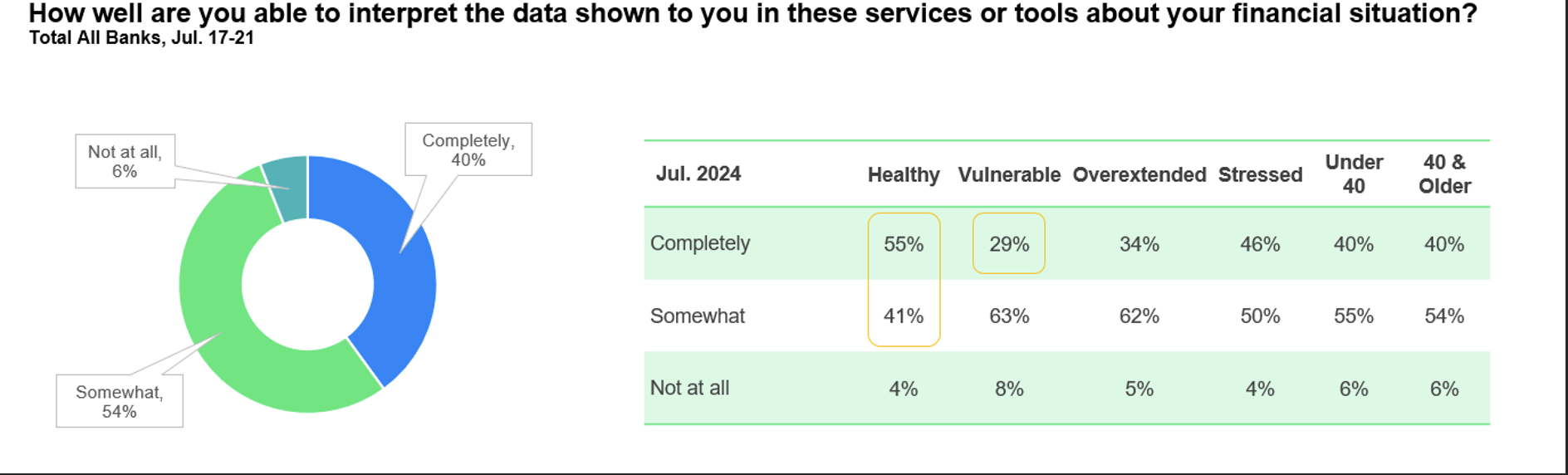

Just 40% of customers said that they completely understand the data presented to them in their bank’s personal financial management tool. This leaves an interpretation gap for more than half of users, which widens as financial health status declines.

When asked specifically if personal financial management tools helped teach them about their money management behaviors, only 29% said these tools helped them completely understand their spending habits. This figure drops to 19% among vulnerable customers.

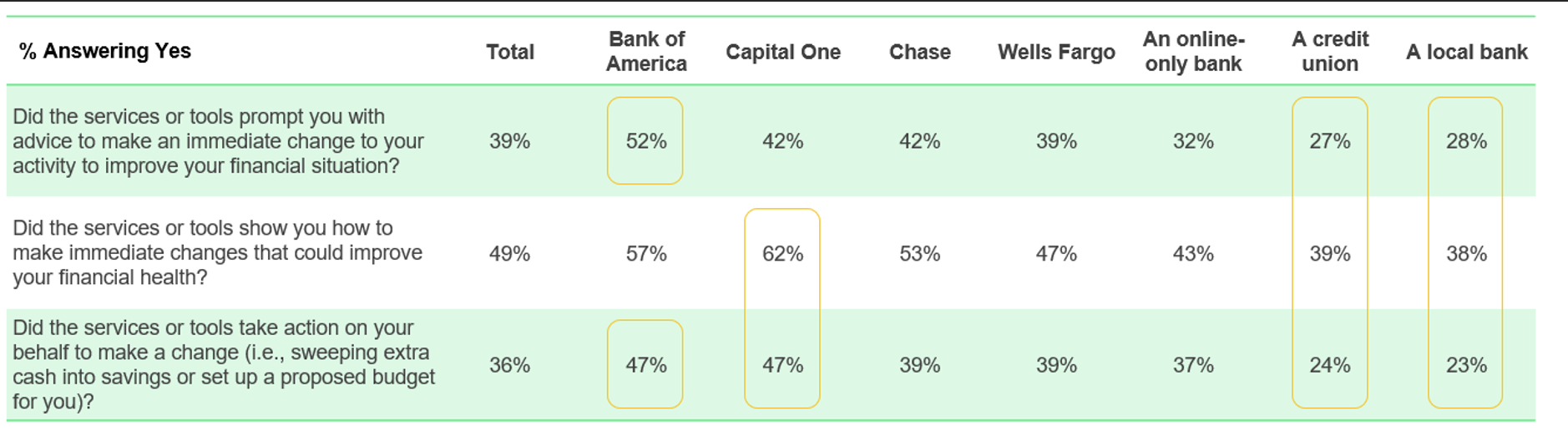

Community banks and credit unions fall behind

Credit unions and local community banks lagged behind large banks and the overall average positive responses in providing actionable steps and the ability to take action on behalf of customers automatically.

Sound like you?

Does your customer/member base feel the same? Do you leverage a more personal and in-person experience to address their financial wellness? The closer proximity and human-centric approach to banking would suggest this is an area of potential advantage to larger and online-only institutions.

Understanding and addressing gaps in experience, where you as a community institution can transcend just a transactional relationship, can be a formidable advantage. It may involve shoring up online tools as part of your digital experience. It may include leaning into a very off-line and person-to-person approach to financial wellness.

Areas of customer experience that are both important to them and present a wide variance in the performance of alternatives can be key differentiators.

For an example of what leaning into financial coaching looks like, not just sales thinly veiled as education, see our discussion with Bree Shellito of Ent Credit Union and her overview of their comprehensive approach.

That’s a wrap for the week. Usually, we throw in something funny here to close things, but today, I’d like to share a touching and thoughtful post from Shaan Puri “Your parents are getting old, here’s what to do”. Call home and have a great weekend. Click below to let us know how we did: